As global heat pump sales seek a new equilibrium, analysts from the International Energy Agency highlight key factors driving investment in manufacturing

Heat pump market trends in 2024

It is still too early to assess the full performance of the 2024 heat pump market. However, early data already provides key insights into production costs and the competitive factors shaping the industry.

The International Energy Agency (IEA) compiled these findings in a commentary published on February 7, offering a deep dive into emerging sector trends.

As previously reported by Rinnovabili, global demand for heat pumps weakened at the start of last year. The European Union— the world’s third-largest market for this technology— saw a 47% drop in sales in the first six months of the year. The main drivers? Shifts in national policies and consumer incentive programs, coupled with falling gas prices that were not matched by a comparable drop in electricity costs.

In the United States, the second-largest market, installations also declined, though by just 1%. Conversely, demand in China grew by 13%, further solidifying the country’s position as the industry leader.

However, a shift may already be underway. Analysts point to early signs of a market rebound. While still preliminary, data from the second half of 2024 suggests a modest recovery, with rising sales in the US, Germany, and Japan.

Where is it cheaper to produce heat pumps?

The IEA also highlights crucial factors for the industry’s recovery, particularly concerning production costs.

Currently, heat pumps are mostly manufactured in the regions where they are installed, with production capacity less geographically concentrated than other clean energy technologies like solar panels or batteries. Despite this, a clear pattern has emerged: most heat pumps sold globally are Made in China.

“China not only holds the largest share of manufacturing capacity for heat pumps but also for key components,” IEA analysts wrote. “In 2023, the country accounted for 95% of global compressor production and 50% of compressors traded worldwide in monetary terms.”

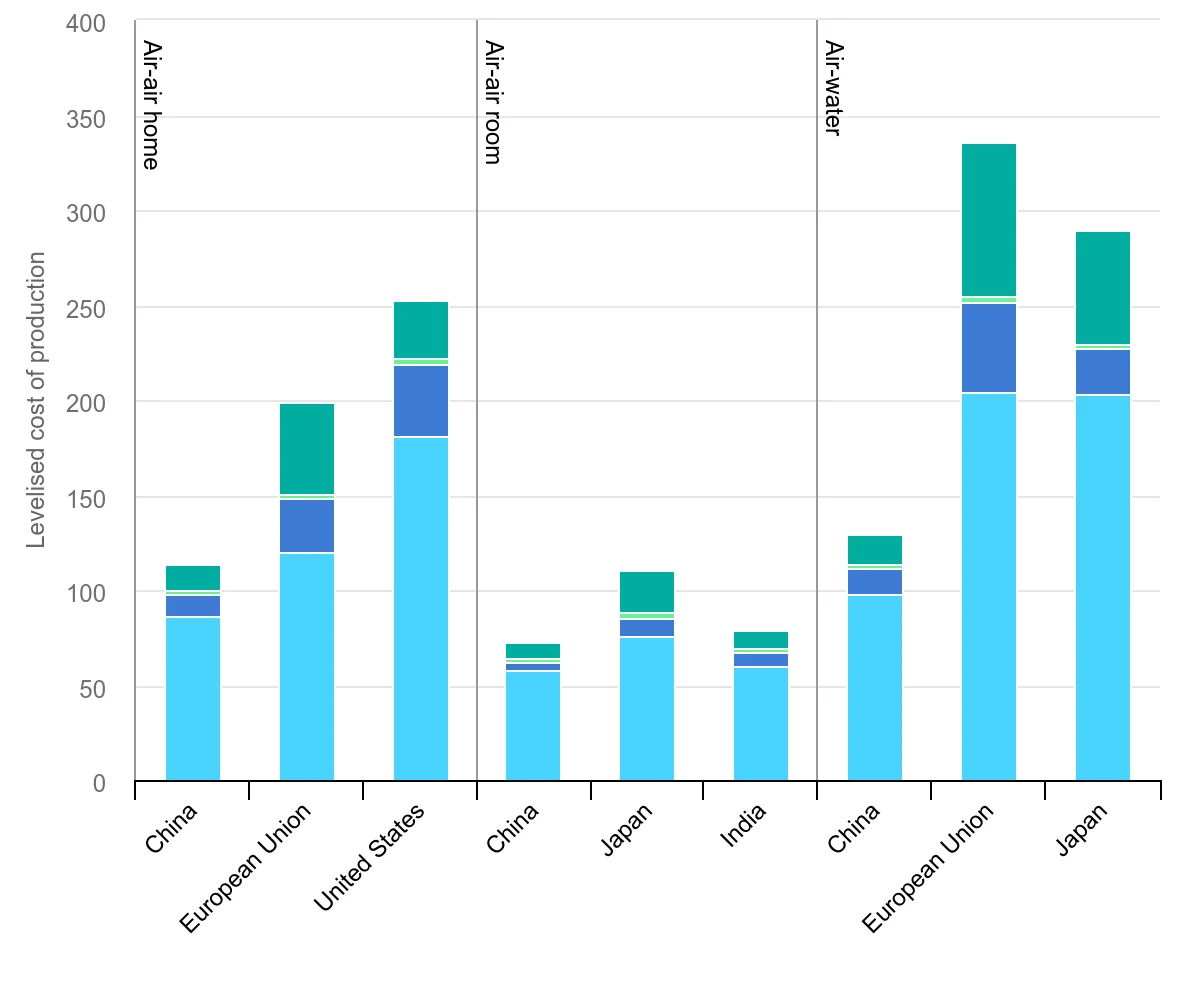

This has a major impact on industrial competitiveness, as reflected in the Levelized Cost of Production (LCOP). LCOP represents the price at which a product must be sold to generate a market-aligned return for investors. Expressed in cost per unit of energy ($/kW), it factors in land, labor, capital, and other expenses.

A comparison of different markets reveals that producing heat pumps in China is 50% cheaper than in the United States and 40-60% cheaper than in the European Union.

“Because heat pump assembly lines are relatively simple and do not require advanced equipment, the capital cost of building factories (which accounts for just 1-3% of LCOP), operational costs for maintaining production lines (10-25%), and labor costs (10-15%) do not significantly contribute to overall production expenses. The primary cost driver is component sourcing (60-80%), meaning companies that can secure in-house components or leverage economies of scale benefit from lower production costs,” the report explains.

Heat pumps and air conditioning: A competitive advantage

Another key factor supporting heat pump manufacturing investments is the synergy with air conditioner production. According to IEA analysts, air conditioning manufacturers have a competitive edge when expanding into the heat pump market compared to companies that exclusively produce heating equipment.

This advantage stems from similar assembly processes and shared key components, such as compressors and heat exchangers. By leveraging existing production capabilities, manufacturers in the air conditioning sector can scale more efficiently and reduce costs when entering the heat pump market.